A loan application is not just about whether you qualify or not. The terms you receive can have a much bigger impact on your finances over time. Two people applying for the same loan amount can end up with very different interest rates, repayment terms, and monthly payments based on how lenders view their financial profile.

Many borrowers focus only on getting approved. However, lenders look at much more than that. They assess risk, repayment capacity, credit behavior, and overall financial stability. Improving these factors before applying can increase your loan eligibility and help you secure better loan terms at a lower cost.

Why Loan Eligibility Matters More Than Most Borrowers Realize

Loan eligibility affects more than approval. It influences the amount you can borrow, the interest rate you receive, and the flexibility of the repayment terms.

Lenders use eligibility criteria to determine how likely you are to repay the loan on time. Borrowers who demonstrate strong financial habits are often rewarded with lower rates because they represent less risk.

Even a small reduction in interest rates can save thousands over the life of a loan. That is why improving your eligibility before applying can be one of the smartest financial moves you make.

Strengthen Your Credit Profile Before Applying

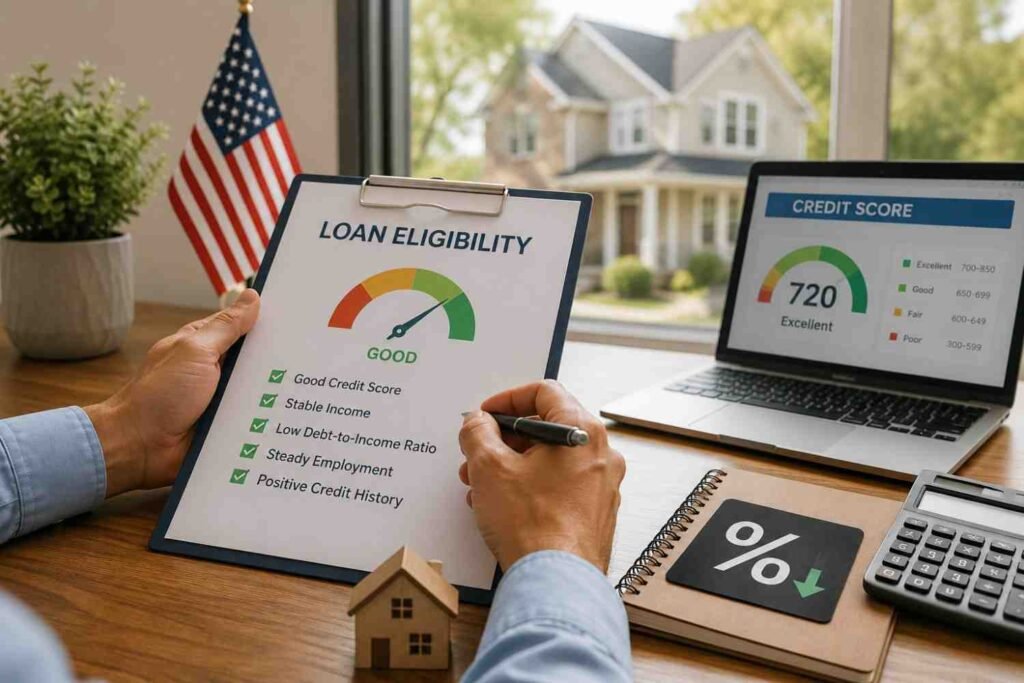

Your credit score remains one of the most important factors in the loan approval process. It provides lenders with a snapshot of your repayment history and overall creditworthiness.

Many lenders reserve their most competitive rates for applicants with credit scores above 750. While reaching that number may take time, several practical steps can help improve your score.

Paying bills on time should be your first priority. A single missed payment can stay on your credit report for years and negatively affect your borrowing capacity. Setting up automatic payments can help eliminate this risk.

Another key factor is credit utilization. Using too much of your available credit can signal financial stress. Keeping your credit utilization ratio below 30% demonstrates responsible credit management and can improve your chances of receiving favorable loan terms.

It is also worth reviewing your credit report regularly. Errors happen more often than many people realize. Incorrect account information or reporting mistakes could lower your score and affect your personal loan eligibility.

Reduce Debt Before Taking On More

One area lenders examine closely is your debt-to-income ratio. This ratio compares your monthly debt obligations to your gross monthly income.

A lower debt-to-income ratio suggests you have sufficient income available to manage new loan payments. Many lenders prefer to see total debt payments remain below 40% of monthly income.

Before submitting a loan application, consider paying off smaller debts or reducing outstanding credit card balances. Even modest improvements can strengthen your financial profile.

This is also where financial borrowing habits become important. Consistently managing debt, avoiding unnecessary borrowing, and maintaining healthy repayment patterns can improve how lenders evaluate your application.

Show Stable and Reliable Income

Income plays a major role in determining loan affordability. Lenders want confidence that your income can comfortably support monthly repayments.

Applicants with stable employment histories often have an advantage because they demonstrate predictable cash flow. Frequent job changes or large income fluctuations can sometimes raise concerns.

If you have multiple income streams, make sure they are properly documented. Freelance work, rental income, consulting income, and investment earnings may strengthen your application when supported by appropriate records.

The goal is to present a complete financial picture rather than relying solely on one income source.

Structure The Loan To Improve Approval Odds

Sometimes, improving loan eligibility is not about earning more money or raising your credit score. It can also involve adjusting how the loan is structured.

Here are a few approaches that lenders often view positively:

- Apply with a co-applicant who has a stable income and strong credit profile.

- Consider secured lending options when appropriate.

- Increase your down payment to reduce the amount being borrowed.

- Select a repayment tenure that balances affordability and total borrowing costs.

These strategies help reduce lender risk, which can improve both eligibility and pricing.

Small Changes Can Lead To Better Loan Terms

Improving loan eligibility rarely happens overnight. Most successful borrowers focus on gradual improvements over several months before applying.

The strongest applications typically share a few common characteristics:

- High credit scores

- Low debt-to-income ratios

- Stable employment history

- Responsible credit utilization

- Limited recent credit inquiries

When these factors work together, lenders often view the applicant as lower risk. That can translate into lower monthly payments, better loan terms, and greater financial flexibility.

FAQs: Ways To Improve Loan Eligibility For Better Loan Terms And Lower Rates

1. Can a higher credit score help me get lower interest rates?

Yes. Lenders generally reserve their most competitive interest rates for borrowers with strong credit scores because they are viewed as less likely to default.

2. What is a good debt-to-income ratio for loan approval?

Many lenders prefer a debt-to-income ratio below 40%, although lower ratios may improve approval chances and help secure better rates.

3. Does applying for multiple loans affect my credit score?

Yes. Multiple hard inquiries within a short period can negatively affect your credit score and may signal a higher risk to lenders.

4. Can a co-applicant improve loan eligibility?

Yes. Adding a co-applicant with stable income and strong credit can increase borrowing capacity and improve approval odds.

Final Thoughts

Improving loan eligibility is not about finding shortcuts. It is about demonstrating financial responsibility in ways that lenders can verify and trust. A stronger credit score, lower debt levels, stable income, and thoughtful application timing all contribute to a healthier financial profile. When lenders see lower risk, they are often willing to offer better interest rates, larger loan amounts, and more flexible repayment options. The effort you put in before applying can create meaningful savings long after the loan is approved.

The best time to improve your eligibility is before you need financing. Small changes today can lead to significantly better borrowing opportunities tomorrow.