Taking out a loan often feels like a solution. Whether you’re covering an unexpected expense, consolidating debt, funding home improvements, or handling a major life event, access to borrowed money can provide relief when you need it most. The challenge is that many people focus on getting approved and overlook what happens after the money arrives.

I’ve seen borrowers spend days comparing lenders but only a few minutes thinking about repayment. That approach can lead to financial stress later. A loan is not just about the amount you borrow. It’s about the commitment you make for months or even years afterward. Understanding the important things to know before taking a loan can help you avoid common mistakes and make a decision that supports your financial goals rather than complicates them.

Start With A Financial Reality Check

Before filling out an application, take a close look at your current financial situation.

The first question should be simple: Do you genuinely need the loan? Borrowing money can make sense for emergencies, education costs, necessary home repairs, or debt consolidation. However, taking on debt for something that can wait may create unnecessary financial pressure.

Next, review your income, expenses, and existing debt obligations. Many borrowers focus only on whether they qualify for a loan. A better question is whether the loan comfortably fits into their monthly budget. If you already feel stretched financially, adding another payment could make things more difficult.

Your credit score also deserves attention. Lenders use it to assess risk, and it often influences the interest rate you receive. A stronger credit profile can save a significant amount of money over the life of the loan.

Understand The Full Cost Of Borrowing

One of the biggest mistakes borrowers make is focusing solely on the interest rate.

The actual cost of a loan includes much more than the advertised rate. Processing fees, origination charges, documentation costs, and late payment penalties can all increase the total amount you pay.

When comparing loan offers, pay attention to:

- Annual Percentage Rate (APR)

- Processing or origination fees

- Late payment charges

- Prepayment penalties

- Documentation fees

Looking at the complete picture helps you compare lenders more accurately and avoid unexpected costs.

Make Sure The Monthly Payment Fits Your Lifestyle

A loan payment might look affordable when viewed in isolation. The real test is whether it fits comfortably within your overall budget.

Think about your regular expenses. Housing costs, utilities, insurance, groceries, transportation, and savings goals all compete for the same income. If a loan payment leaves little room for flexibility, even a minor financial setback can create problems.

Before borrowing, calculate exactly how much you will owe each month. Then ask yourself an important question: Would you still be able to manage this payment if an unexpected expense appeared next month?

Being honest with yourself during this step can prevent future financial strain.

Choose The Right Loan Term

The repayment period affects both your monthly payment and the total amount you repay.

A shorter loan term typically results in higher monthly payments but lower overall interest costs. A longer term often reduces the monthly payment but increases the total amount paid over time.

Many borrowers automatically choose the longest available term because it appears more affordable. While lower payments can be helpful, extending the loan unnecessarily may cost substantially more in interest.

The best option is usually the shortest repayment period that comfortably fits your budget without creating stress.

Know Whether You’re Taking A Fixed Or Variable Rate Loan

Not every loan works the same way.

A fixed-rate loan keeps the interest rate consistent throughout the repayment period. This makes budgeting easier because monthly payments remain predictable.

A variable-rate loan can change over time based on market conditions. While the initial rate may be attractive, future increases could result in higher payments.

Understanding the difference before signing any agreement is essential. Many borrowers pay attention to the starting rate but fail to consider how future rate changes might affect their finances.

Borrow Only From Trusted Lenders

The lender matters just as much as the loan itself.

A reputable lender should clearly explain interest rates, fees, repayment schedules, and borrower responsibilities. Transparency is usually a sign of credibility.

Take time to compare multiple lenders rather than accepting the first offer available. Read reviews, verify credentials, and make sure all terms are clearly documented.

Be cautious if a lender guarantees approval, pressures you to act immediately, or avoids answering questions about fees and repayment terms. These are often warning signs that deserve closer attention.

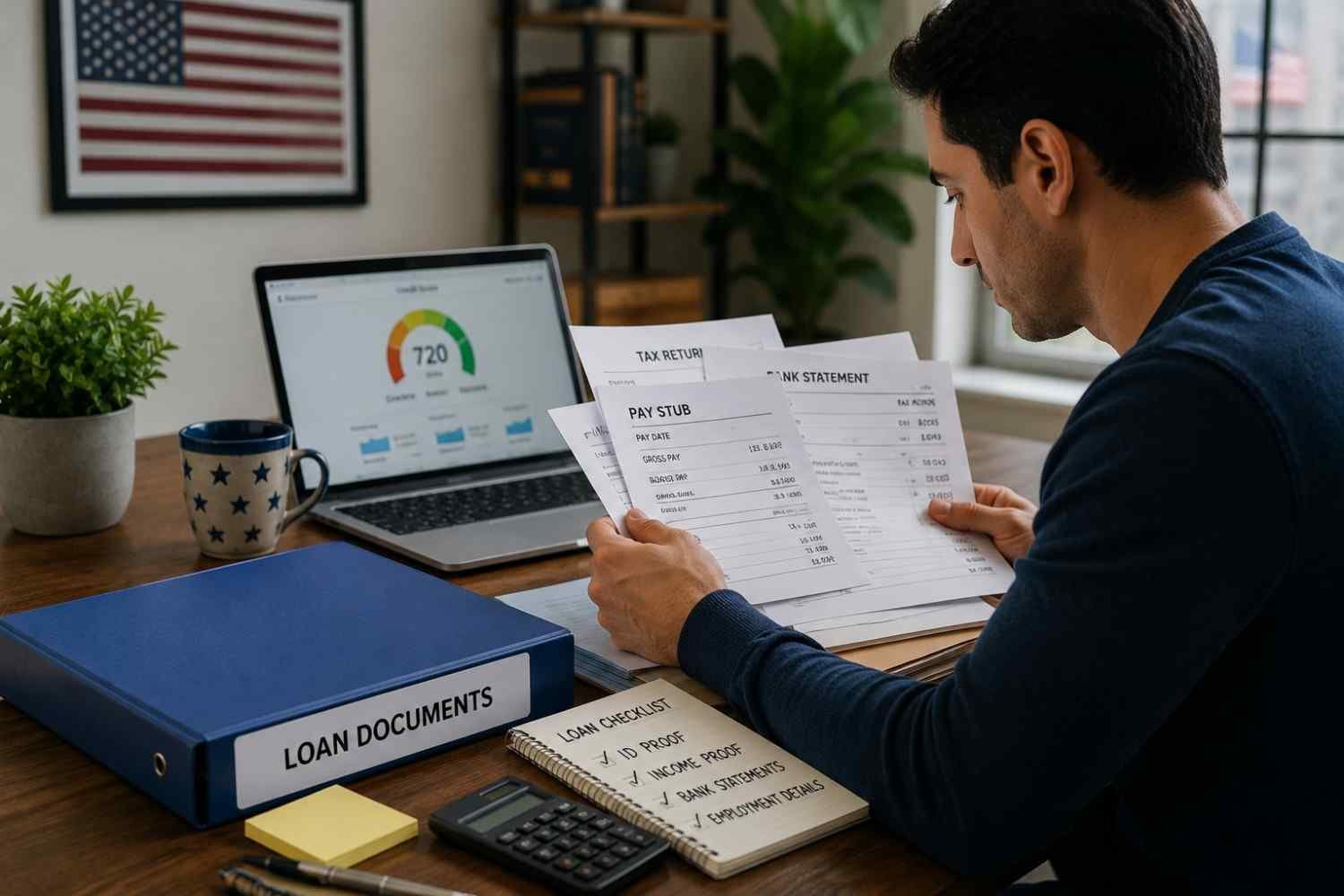

Prepare Your Documents Before Applying

A well-prepared application process can save time and reduce frustration.

Most lenders require documentation that verifies your identity, income, and financial history. Gathering these documents in advance helps streamline the approval process and demonstrates financial responsibility.

Common requirements often include proof of identity, income verification, tax documents, employment information, and recent bank statements.

Having everything organized before applying can prevent unnecessary delays.

Improve Your Position Before You Apply

Many people rush into submitting a loan application as soon as they decide they need financing. In some cases, waiting a few weeks can lead to a better outcome.

If you’re exploring ways to improve loan eligibility, consider paying down existing debt, correcting errors on your credit report, avoiding unnecessary credit inquiries, and maintaining a strong payment history. Small improvements can make a meaningful difference when lenders evaluate your application.

A little preparation before applying can often lead to better loan terms and potentially lower borrowing costs.

FAQs: Things To Know Before Taking A Loan: A Practical Borrower’s Checklist

1. What is the most important thing to know before taking a loan?

The most important factor is your ability to repay the loan comfortably. Before borrowing, review your budget, income stability, and existing financial obligations.

2. Why is a credit score important when applying for a loan?

Your credit score helps lenders assess risk. A higher score often improves approval chances and may help you qualify for more favorable interest rates.

3. Should I choose a shorter or longer loan term?

A shorter term generally reduces total interest costs but increases monthly payments. A longer term lowers monthly payments but usually costs more overall.

4. Can I pay off a loan early?

Many loans allow early repayment, but some lenders charge prepayment or foreclosure penalties. Always review the loan terms before signing.

Final Thoughts

Borrowing money is not inherently good or bad. It is simply a financial tool. The key is knowing how to use that tool responsibly. Taking time to evaluate your financial situation, understand the true cost of borrowing, compare lenders, and review loan terms carefully can help you make a decision that supports your long-term financial health. The best borrowers are not necessarily the ones who qualify for the largest loans. They are the ones who understand exactly what they are committing to before signing the agreement.

A little preparation today can help you avoid costly mistakes tomorrow. Smart borrowing begins with informed decision-making.