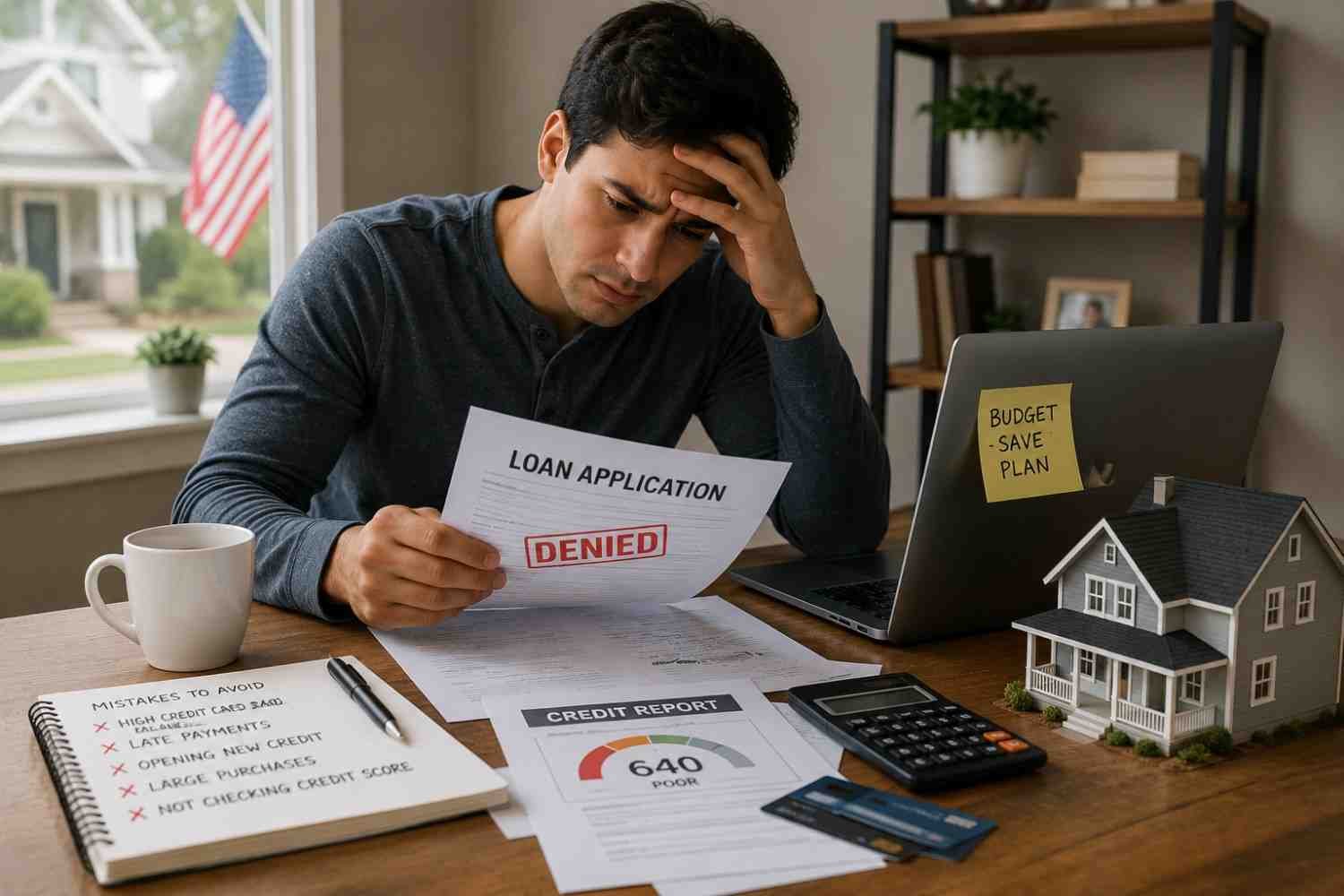

Taking out a loan for the first time can feel like a major financial step. Many people reach a point where they need extra funds for home improvements, medical expenses, debt consolidation, education costs, or other unexpected situations. A personal loan often appears to be a straightforward solution, but the process can seem confusing when you’re unfamiliar with lending terms, eligibility requirements, and repayment obligations.

I remember speaking with several first-time borrowers who focused only on getting approved. What they later realized was that approval is just one part of the process. Understanding how personal loans work, how lenders assess applications, and how repayments fit into your monthly budget is what truly helps you make a smart borrowing decision. This personal loan guide covers the essentials every first-time borrower should know before applying.

What Is a Personal Loan?

A personal loan provides immediate access to funds that you repay through fixed monthly payments over a predetermined period. Unlike secured loans, most personal loans do not require collateral such as a home, vehicle, or savings account.

Because these loans are unsecured, lenders evaluate your application based on your financial profile. Factors such as income, employment stability, credit history, and existing debt obligations play a significant role in the approval process.

Many borrowers use personal loans for:

- Emergency expenses

- Home repairs and renovations

- Medical bills

- Debt consolidation

- Major purchases

- Wedding expenses

- Educational costs

The flexibility of an unsecured personal loan makes it attractive, but that flexibility also means borrowers need to be disciplined about repayment.

Understanding Personal Loan Eligibility

Before submitting a personal loan application, it helps to understand the criteria lenders commonly use to evaluate borrowers.

Age Requirements

Most lenders prefer applicants between 21 and 60 years old. Some institutions may have slightly different age limits, but this range remains common across the industry.

Credit Score Matters

Your credit score is one of the most important factors in the loan approval process. A strong credit history demonstrates that you have managed debt responsibly in the past.

Generally, scores above 710 to 750 help borrowers qualify for better personal loan interest rates and more favorable loan terms.

Income and Employment Stability

Lenders want reassurance that you can comfortably handle monthly loan payments. Stable employment and consistent income often improve approval chances.

Many lenders require minimum monthly earnings that meet specific thresholds. Beyond income, they also review your debt-to-income ratio to determine affordability.

Existing Financial Obligations

Even borrowers with strong incomes may face challenges if they already carry significant debt. Lenders examine your current financial commitments to ensure additional borrowing remains manageable.

Documents You Should Prepare Before Applying

One of the easiest ways to avoid delays is to gather required documents before starting the application process.

Identity Verification

Common identification documents include:

- PAN card

- Aadhaar card

- Passport

- Other government-issued identification

Address Verification

Lenders may request:

- Utility bills

- Rental agreements

- Driver’s license

- Official address documentation

Income Verification

To confirm repayment capacity, lenders often require:

- Recent salary slips

- Tax returns

- Employment verification documents

Banking Records

Bank statements covering the previous six months help lenders evaluate income patterns and spending behavior.

Having these documents organized beforehand can make the process smoother and reduce approval delays.

Key Loan Terms Every Borrower Should Understand

Many first-time borrowers sign agreements without fully understanding the terminology. Learning a few basic terms can help you compare loan offers more effectively.

Equated Monthly Installment (EMI)

The EMI represents the fixed monthly amount you pay throughout the loan tenure. It includes both principal repayment and interest costs.

Loan Tenure

Loan tenure refers to the repayment period. Personal loans commonly range from 12 to 48 months, although some lenders offer longer terms.

A longer tenure may reduce monthly payments but can increase total interest costs over time.

Processing Fees

Most lenders charge a processing fee to review and manage your application. This fee is typically deducted before funds are disbursed.

Annual Percentage Rate (APR)

APR provides a broader picture of borrowing costs because it includes interest rates and applicable fees. Comparing APRs often gives a more accurate comparison than looking at interest rates alone.

How to Choose the Right Personal Loan

Many first-time borrowers focus exclusively on interest rates. While rates matter, they should not be the only factor guiding your decision.

Consider these factors when comparing lenders:

- Total borrowing cost

- APR and processing fees

- Loan tenure flexibility

- Prepayment penalties

- Customer support quality

- Repayment options

- Approval timelines

The lowest advertised rate does not always result in the most affordable loan. Looking at the complete picture helps avoid unpleasant surprises later.

The Personal Loan Application Process

Applying for a personal loan has become much simpler thanks to digital lending platforms and online verification systems.

Step 1: Calculate Your Repayment Capacity

Before borrowing, determine how much you can comfortably repay each month without straining your finances.

Step 2: Review Your Credit Report

Check for errors, outdated information, or inaccuracies that could affect your credit score.

Step 3: Compare Loan Offers

Evaluate multiple lenders before making a decision. Comparing offers can reveal significant differences in fees and loan terms.

Step 4: Gather Documents

Preparing documentation in advance speeds up the review process.

Step 5: Submit Your Application

Most lenders now offer online applications that can be completed in minutes.

Step 6: Complete Verification

Digital KYC and identity verification help lenders validate information quickly.

Step 7: Review and Sign

Carefully read the agreement before signing. Pay close attention to fees, repayment schedules, and penalty clauses.

Common Mistakes First-Time Borrowers Should Avoid

Many financial challenges arise not from borrowing itself but from borrowing incorrectly.

Borrowing More Than Necessary

A larger loan may seem appealing, but every additional dollar borrowed increases interest costs and repayment obligations.

Applying to Too Many Lenders

Submitting multiple applications within a short period can negatively affect your credit profile and create unnecessary complications.

Ignoring Affordability Limits

Financial experts often recommend keeping total debt payments below roughly 40% of monthly income. Exceeding that level can make repayment difficult.

Skipping the Fine Print

Processing fees, late payment charges, and prepayment penalties can significantly affect the overall cost of borrowing.

Neglecting Repayment Planning

A successful loan experience depends heavily on responsible loan management. Setting up automatic payments, maintaining an emergency fund, and monitoring your repayment schedule can help prevent missed payments and unnecessary fees.

Frequently Asked Questions: The Complete Personal Loan Guide for First-Time Borrowers

1. Can I get a personal loan with a fair credit score?

Yes. Some lenders approve borrowers with fair credit scores, although interest rates may be higher than those offered to applicants with stronger credit profiles.

2. How long does personal loan approval usually take?

Many online lenders provide approval decisions within a few hours or a few business days, depending on document verification requirements.

3. Is a personal loan better than using a credit card?

It depends on the situation. Personal loans often provide fixed repayment schedules and predictable monthly payments, while credit cards offer revolving credit with variable repayment periods.

4. Can I repay a personal loan early?

Many lenders allow early repayment, but some charge prepayment penalties. Always review loan terms before signing an agreement.

Final Thoughts

A personal loan can be a useful financial tool when used thoughtfully. The key is not simply getting approved but understanding how the loan fits into your broader financial goals. First-time borrowers often focus on interest rates alone, yet factors like repayment capacity, loan tenure, fees, and long-term affordability are equally important. Taking the time to compare offers, review your budget, and understand loan terms can make a significant difference in your overall borrowing experience.

Borrow carefully, repay consistently, and treat every borrowing decision as part of a larger financial plan. Doing so can help you gain the benefits of a personal loan without creating unnecessary financial stress.