I used to think budgeting failed because I lacked discipline. The real problem was timing. My bills, spending, savings, and payday were not working from the same calendar.

That is why paycheck budgeting tips can work better than a broad monthly budget. Instead of guessing what you can spend this month, you plan what each paycheck must do before the next one arrives.

Paycheck budgeting means assigning one specific paycheck to bills, savings, debt, and daily spending. It works well for weekly, bi-weekly, semi-monthly, and monthly pay cycles because it focuses on cash flow, not wishful thinking.

The Consumer Financial Protection Bureau recommends mapping income dates beside bill due dates to manage cash flow more clearly. That same idea sits at the center of this method.

Why Paycheck Budgeting Works When Regular Budgets Fail

A regular monthly budget can look perfect on paper and still fail by the 20th. Why? Because it may not show when money leaves your account.

Paycheck budgeting fixes that gap. It answers three practical questions:

When do I get paid?

Which bills must this paycheck cover?

How much can I safely spend before the next pay date?

The CFPB also notes that a realistic budget helps you understand money coming in, money going out, and what may be left for savings goals.

In my experience, the biggest win is emotional. When I know a bill is already assigned to a paycheck, I stop mentally spending the same money twice.

Start by Matching Pay Dates With Bill Due Dates

Map Income Before Expenses

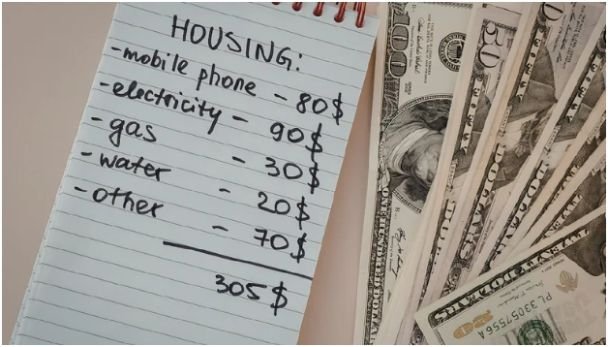

Open a calendar and mark every pay date first. Then add rent, mortgage, utilities, insurance, credit cards, loan payments, subscriptions, and childcare costs.

Do not estimate due dates. Use exact dates.

If your paycheck arrives on the 5th and your car payment is due on the 9th, that bill belongs to that paycheck. If your electric bill is due on the 24th, it may belong to the next paycheck.

This simple map gives you a cleaner way to balance income and expenses without relying on memory.

Assign Bills to the Right Paycheck

Once your calendar is clear, group bills by paycheck. The goal is to stop treating your bank balance as spendable money.

For example, if your take-home pay is $2,000 on the 1st and rent is $1,200 due on the 3rd, that $1,200 is already gone. Your real budget begins after that.

This step feels strict at first, but it prevents the classic mistake: spending freely after payday, then scrambling before due dates.

Split Large Monthly Bills Before They Hit

Use a Half-and-Hold System

Large bills create pressure when they land on one paycheck. Rent, mortgage, car payments, insurance premiums, and tuition can drain your account fast.

If rent is $1,600 and you are paid bi-weekly, hold $800 from the first paycheck and $800 from the second. When rent is due, the full amount is ready.

This method works best when the first half sits in a separate savings bucket or bills account. Do not leave it mixed with grocery and entertainment money.

Keep Big Bills Away From Daily Spending

I like to treat bill money as unavailable. Once it is assigned, I move it away from my spending account.

That small friction matters. When money sits in one account, it feels spendable. When it sits in a bills account, it feels protected.

Use Zero-Based Budgeting for Each Paycheck

Give Every Dollar a Job

Zero-based budgeting means your paycheck minus expenses, savings, debt, and spending equals zero. It does not mean you spend everything. It means every dollar has a purpose.

A paycheck plan may include:

Fixed bills

Groceries

Gas

Debt payments

Emergency savings

Fun money

Buffer money

The FDIC’s Money Smart program teaches budgeting around income, expenses, savings, and the “pay yourself first” concept. That supports the idea of saving before casual spending takes over.

A Simple Paycheck Budget Example

Imagine your bi-weekly take-home pay is $2,200.

You assign $900 to rent savings, $250 to utilities and phone, $150 to car insurance, $400 to groceries and gas, $200 to debt, $200 to savings, and $100 to personal spending.

Your paycheck now equals zero on paper, but your life has room to breathe. Bills are covered, savings moved, and spending has a clear limit.

This is one of the most useful paycheck budgeting tips because it removes vague money decisions.

Separate Your Money So You Do Not Overspend

Bills Account

Use one checking account for fixed bills only. Rent, mortgage, utilities, insurance, loan payments, and subscriptions should come from here.

Keep autopay bills in this account so you do not accidentally spend bill money on daily purchases.

Spending Account

Use a second account for groceries, gas, dining out, and personal spending. This account shows what you can actually use.

When it runs low, you slow down. You do not borrow from rent or savings.

Savings Account

Route savings to a separate account as soon as you get paid. A high-yield savings account can help keep emergency money away from daily spending.

The FDIC recommends reviewing recent spending, cutting recurring costs where possible, and creating a monthly spending and saving plan.

Build a Small Buffer Before You Chase Bigger Goals

A buffer is not the same as a full emergency fund. It is a small cushion that protects you from timing problems.

For US readers, a starter buffer of $100 to $500 can prevent overdrafts. Once that feels stable, build toward one month of expenses.

Treat the buffer as zero. If your account has $300 and your buffer rule is $250, you only have $50 available.

This protects you when autopay clears early, gas costs more than expected, or a paycheck posts later in the day.

Paycheck Budgeting Tips for Monthly Earners

Create a 4-Week Internal Paycheck

Monthly pay needs a different rhythm. The danger is feeling rich in week one and broke in week four.

When your salary lands, pay fixed costs first. Then move savings immediately. After that, divide the remaining spending money by four.

If $1,600 remains for groceries, gas, dining, and shopping, your weekly spending limit is $400. Release only one weekly portion at a time.

This creates an internal paycheck system. You get paid once, but you manage money as if you receive four smaller checks.

Move Bill Dates Near Payday

A monthly paycheck gives you leverage. Ask credit card issuers, insurance companies, and lenders whether you can shift due dates.

The CFPB says adjusting bill due dates can help people stay on top of bills and manage cash flow.

For monthly earners, I prefer due dates between the 3rd and 7th. That clears major bills while the account balance is highest. After that, the remaining money is easier to pace.

Use Budgeting Apps Without Losing Control

Best App Types for Paycheck Budgeting

Budgeting apps can make paycheck planning easier, but the best choice depends on your style.

Goodbudget works well for digital envelope budgeting. You fill envelopes like groceries, gas, bills, and savings. Manual entry makes you more aware of spending.

Automated tracking apps help when you dislike manual work. They categorize card and bank activity, then show spending patterns.

Spreadsheet-style apps work for households that need more detail. They help track multiple accounts, credit cards, assets, and shared expenses.

Investment-linked apps can help move leftover money into savings or investing goals. Use them only after bills, debt minimums, and emergency savings are handled.

Security Rules Before Syncing Financial Data

Before using any budgeting app, review permissions. Avoid apps that ask for banking passwords, PINs, or security codes.

The FTC advises strong account protection, including better password habits and two-factor authentication.

Use biometric lock or a master passcode inside the app. Also check whether the app reads only financial alerts or has broader access than needed.

Convenience is helpful. Blind access is not.

Common Paycheck Budgeting Mistakes to Avoid

The first mistake is budgeting from gross income. Always use take-home pay after taxes, insurance, and retirement deductions.

The second mistake is ignoring irregular expenses. Car registration, holiday gifts, annual subscriptions, and school costs still count. Divide yearly costs by 12 and save monthly.

The third mistake is making spending categories too tight. A budget that leaves no room for real life will break quickly.

The fourth mistake is skipping fun money. Even $20 per paycheck gives you a guilt-free outlet.

The fifth mistake is checking your bank balance instead of your budget. Your balance shows what exists. Your budget shows what is available.

FAQs About Paycheck Budgeting Tips

1. What is the best way to budget each paycheck?

Assign bills first, move savings next, set spending limits, and give every dollar a job before spending.

2. How do I budget if I live paycheck to paycheck?

Start with due dates, cover essentials first, build a small buffer, and split large bills across paychecks.

3. Is paycheck budgeting better than monthly budgeting?

It can be better if your main problem is timing, overspending after payday, or missing bill due dates.

4. What app is best for paycheck budgeting?

Envelope apps suit manual budgeters, while automated tracking apps suit people who want spending alerts and category summaries.

Final Take: Make Payday Behave

Payday should not feel like a short celebration followed by three weeks of stress. The fix is not always earning more. Sometimes it is giving your paycheck better instructions.

The best paycheck budgeting tips are simple: map your pay dates, assign bills early, split large costs, move savings first, separate spending money, and protect your buffer. Once your paycheck has a plan, your bank balance stops lying to you.

Start with your next paycheck only. Do not rebuild your whole financial life in one sitting. Plan one pay cycle well, then repeat it until payday finally starts acting right.